Roof Depreciation Rate

Part Three The Value Of Accurate Roof Age In Claims

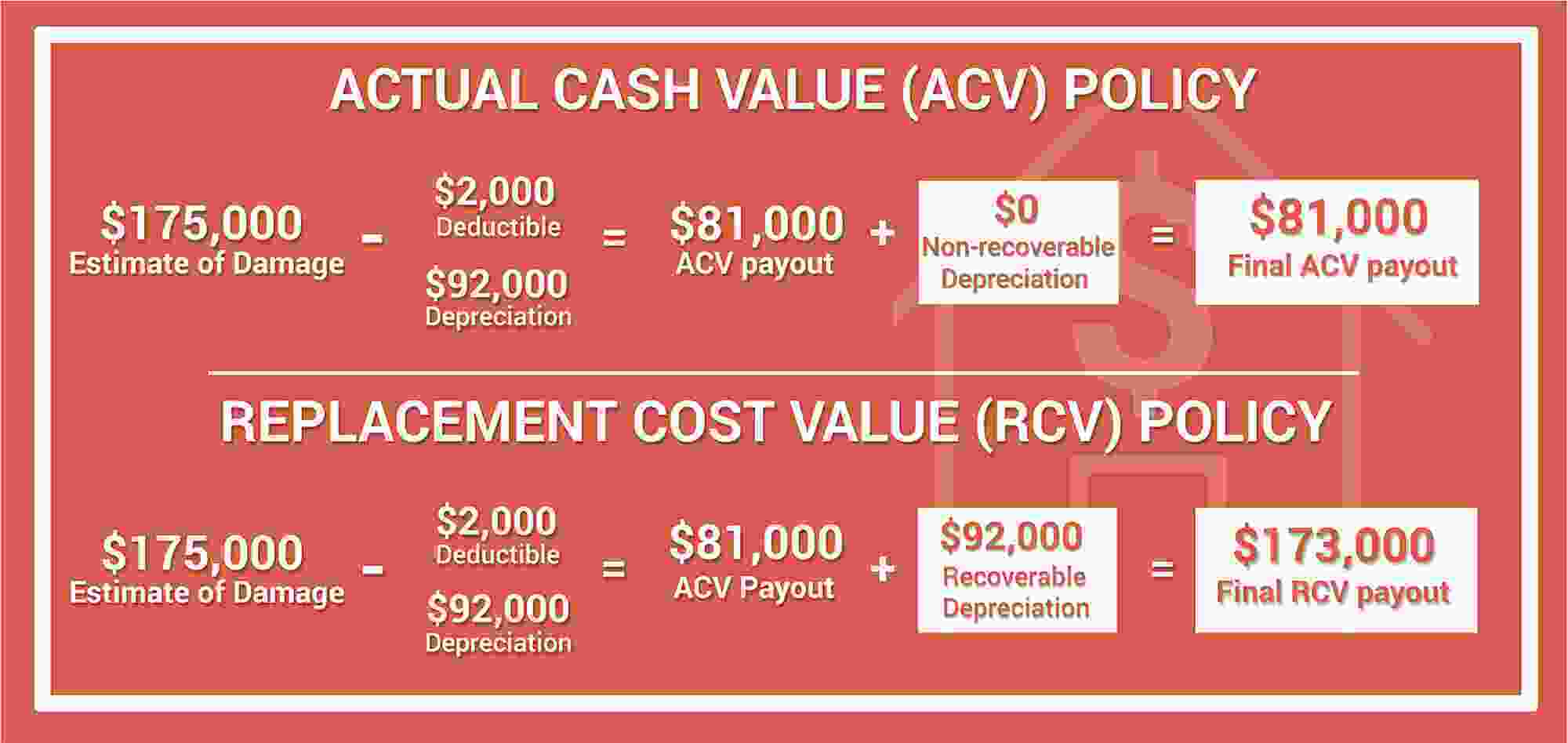

What Recoverable Depreciation Means And How To Calculate It

Replacement Cost Value Rcv Vs Actual Cash Value Acv

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

How To Understand Depreciation On Your Roof Insurance Claim

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

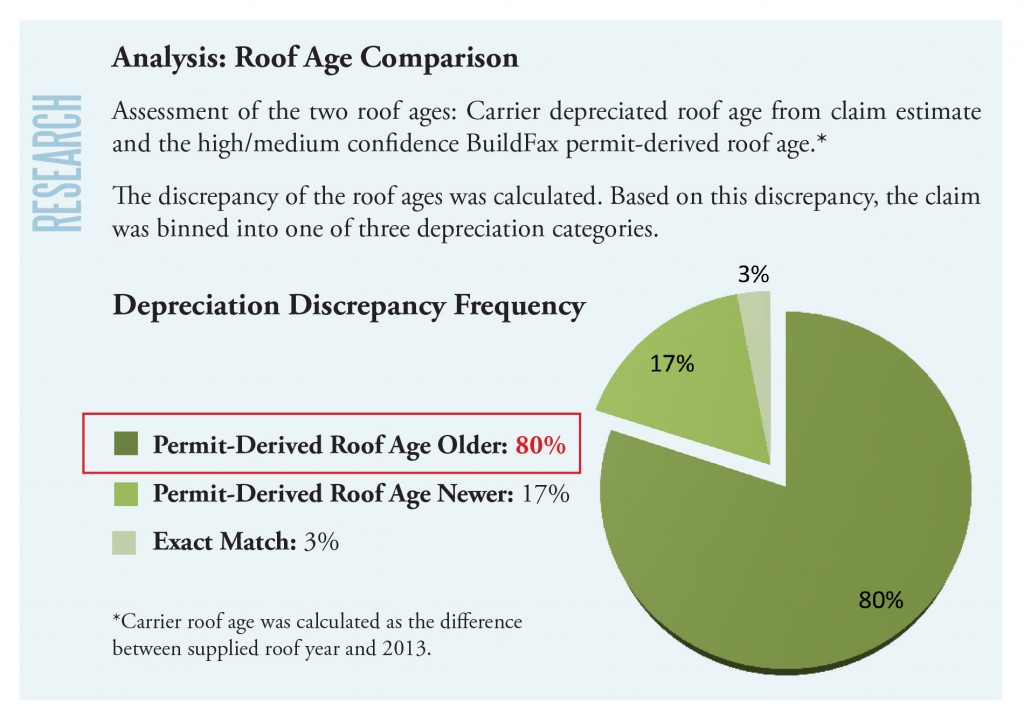

For instance a brand new composition shingle roof may depreciate at a published rate of 2 to 3 per year until it reaches a certain minimum amount say 25.

Roof depreciation rate.

How Recoverable Depreciation Works

Actual Cash Value The 15 Year Roof Rule Cw Roofing Construction

Acv Vs Rcv Office Of Public Insurance Counsel Opic

What Is The Depreciation Of The Roof On A Commercial Building

How The New Tax Law Affects Rental Real Estate Owners Mitchell Wiggins

The Average Depreciation Rate Of A Vehicle Small Business Chron Com

How Rental Property Depreciation Works The Benefits To You

Give Me My Recoverable Depreciation

How The New Tax Law Affects Rental Real Estate Owners

12762 Increasing Basis On An Asset Being Depreciated

Roof Insurance Acv Vs Replacement Cost Bankrate

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin

Homeowners Insurance 101 Roof Age Matters At Claim Time

How To Get Your Homeowners Insurance To Pay For Roof Replacement

Section 179d Tax Deduction For Commercial Roof Replacements

Health Depreciation Rate With Age And Health Investment Download Scientific Diagram

Roof Deductible L Depreciation L Roof Insurance Claim Specialists Bbr Contracting Residential Commercial Roofing Services

Heatspring Magazine Finance 101 For Solar Pv Professionals

Actual Cash Value Is The Cost Of Labor Part Of Depreciation The Courts Are Divided Insurance And Reinsurance Disputes Blog

Rental Property Depreciation Rules Schedule Recapture

Can I Make Money Off My Insurance Roofing Claim Slade Roofing

The 2020 Ultimate Guide To Irs Schedule E For Real Estate Investors

What Exactly Is Actual Cash Value Expert Commentary Irmi Com

What Is Rental Property Depreciation And How Does It Work

Source : pinterest.com